Jeremy Goro leads financial services strategy and partnerships at Google. A thought leader in the space, he recently co-authored AI’s Next Frontier for Financial Services Leaders alongside finance experts from Oliver Wyman, Innovate Finance, and Google, detailing the industry’s shift toward agentic AI.

The United Arab Emirates (UAE) is experiencing a wave of agentic AI adoption, with the technology poised to become a core engine for growth across both public and private sectors. Unlike traditional automation, these intelligent systems plan, decide, and autonomously execute complex, multi-step workflows on behalf of customers and employees. While no industry is untouched, banks and fintechs will stand at the absolute epicentre of this transformation.

“As AI evolves from providing basic assistance to taking autonomous action, it’s poised to fundamentally reshape the future of financial services in the Middle East and the rest of the world,” explains Adrian Oest, partner at consultancy firm Oliver Wyman. “In this new landscape, marketing teams pivot from manual execution to strategic architects, managing AI agents that deliver hyper-personalised experiences at a scale previously reserved for science fiction.”

In our latest white paper report, “AI’s Next Frontier for Financial Services Leaders”, written in collaboration with Oliver Wyman and Innovate Finance, we analyse the key growth drivers behind this rapid shift, and explore the new economic realities emerging as agentic AI takes the wheel.

AI is moving from helping to doing

We’re transitioning from the first wave of generative AI to a second wave of agentic AI. And the appetite is clearly there. An Oliver Wyman survey reveals that over 80% of financial services professionals already express a willingness to treat an AI agent as a “co-worker”.1

Today, your marketing team might ask an AI assistant to summarise dense market research. Tomorrow, a single prompt will trigger an AI agent to design, build, and launch an entire campaign from scratch.

Tools like the personal AI agent Gemini Spark are already driving this transition by operating in the background without needing people’s attention. This allows teams to automate complex, multi-step workflows, like automating continuous data monitoring, freeing up time for high-level strategy.

Andy Thornley, head of regulatory affairs at fintech industry body, Innovate Finance, says this shift will change how financial institutions operate. “By embedding AI agents directly into real customer journeys, banks and fintechs can profitably unlock underserved market segments and offer consumers automated guidance on complex, historically gated financial decisions, further democratising financial advice.”

This agentic reality is powered by major tech leaps. Today’s large language models (LLMs) have much sharper reasoning, although humans still need to oversee complex financial choices. Expanding context windows can digest mountains of data, making it more valuable, while advanced memory recalls user preferences over time.

Ultimately, these breakthroughs unlock autonomous action, allowing AI agents to securely connect to external systems and regulated financial models to execute real-world tasks on their own.

Today, your marketing team might ask an AI assistant to summarise dense market research. Tomorrow, a single prompt will trigger an AI agent to design, build, and launch an entire campaign from scratch.

A dual strategy for incumbent banks and fintechs

Our research shows that incumbent banks have used their deep pockets to successfully pilot AI, scoring major wins in back-office efficiencies. Executives currently deploy intelligent agents to streamline ID verification, automate compliance reviews, and optimise marketing analytics.

Meanwhile, digital-native fintechs have the agility to embed agentic AI across their entire value chain to deliver customer-facing advances. Because the public expects fintechs to be experimental, they have the freedom to test, iterate, and disrupt without the constraints traditional banks face.

Financial infrastructure tech company, Stripe, for instance, operates its AI-run Payments Foundation Model (PFM) across a massive scale, optimising flows and detecting fraud across the company’s total annual processing volume, which reached $1.9 trillion USD last year. Demonstrating how rapidly fintechs can scale AI innovations, Stripe also recently announced a major partnership with Google, launching merchant checkout capabilities that allow businesses to sell directly to consumers inside AI Mode and Gemini.

Ultimately, unlocking agentic AI across the finance ecosystem requires scalable cloud infrastructure, supportive regulation, secure identity verification, and the trust to let AI work autonomously.

3 distinct AI economies are coming

Our research suggests that the widespread adoption of agentic AI will give rise to three distinct economies, presenting fresh opportunities for finance brands to unlock new sources of value:

1. Agentic-twin economy

Readiness for AI agents is at an all-time high. However, a major bottleneck remains: customer data is fragmented across a sea of apps, leaving banks with outdated snapshots of their customers rather than the holistic view required for a seamless “assistance economy”.

Enter agentic twins. Owned by the consumer, these personal AI assistants securely store aggregated data and digital identities under predefined permissions. They will evolve from managing passwords and calendars to handling complex product selection and provider interfacing in the background. This shifts the paradigm from inefficient data chasing to secure, permissioned collaboration, enabling richer content-driven insights and faster interactions.

Simplifying the experience for both customers and providers opens the door to some powerful new opportunities. Oest says agentic twins can offer hyper-personalised, rational financial assistance at scale, with this newfound transparency setting up customers for greater success.

Additionally, Thornley adds that future revenue growth will rely heavily on becoming the top choice of these digital counterparts. He says: “To stand out, finance companies will need to engage these AI assistants through clear, logic-driven communication that aligns with the AI’s twins’ programmed values. This approach complements traditional marketing creativity with data-backed precision that these systems need.”

Naturally, this shift brings security to the forefront. Because AI twins act as a protective shield for the customer, banks and fintechs must be completely transparent about fees and prove strict privacy compliance to earn trust. Institutions that pioneer robust authentication and restore data ownership will gain a massive competitive edge.

By putting control back in the customers’ hands and earning consent through real, demonstrable value, data transforms into a shared asset, elevating consumers from passive users into active partners in their financial journey.

2. The assistance economy

We’re already seeing glimpses of assistance economy models rolling out in the banking sector, most notably with Citi Wealth’s unveiling of Citi Sky. Developed on Google Cloud using the Gemini Enterprise Agent Platform and Google DeepMind’s frontier models, Citi Sky functions as an always-on, AI-powered member of the wealth team. Leveraging Google DeepMind’s real-time digital avatar technology alongside Gemini’s live audio and video models, the platform moves beyond traditional banking interfaces toward fluid, conversational intelligence. By offering financial guidance and support, enabling customers to instantly act on advice, it highlights how quickly large-scale financial institutions are recognising and scaling sophisticated agentic technology.

We are seeing a similar rapid scaling of agentic tech on the institutional side with Deutsche Bank’s rollout of DB Lumina. Developed with Google Cloud using Vertex AI and Gemini models, DB Lumina serves as an intelligent research assistant for the bank’s global analysts. Through conversational chat, analysts can query complex documents, translate insights, and summarise massive reports. Secured by a Retrieval-Augmented Generation (RAG) architecture, the platform cross-references queries with internal databases, central bank data, and global filings to ensure responses are grounded in verified facts. This allows it to track deep trends, like scoring central bank sentiment, complete with verifiable inline citations. By shifting teams from manual data gathering to high-level strategy, it underscores just how deeply large-scale banking is embedding generative AI into core workflows.

As this landscape matures, we expect to see distinct types of agentic models emerge to define user behaviour.

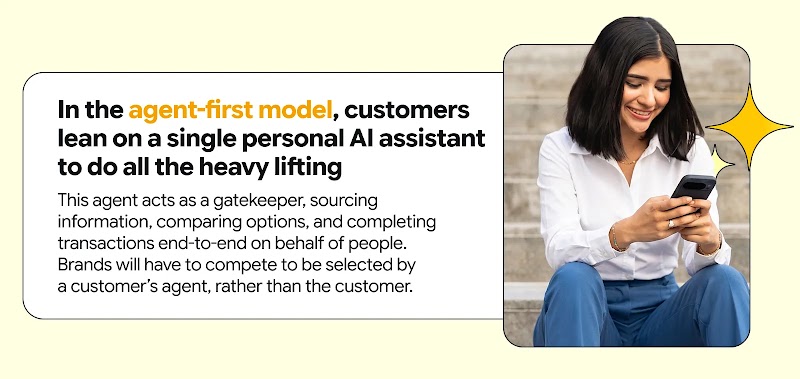

“In the agent-first model, consumers can lean on a single personal AI assistant to do all the heavy lifting,” Oest says. “This agent acts as a gatekeeper, sourcing information, comparing options, and completing transactions end-to-end on their behalf. Brands will have to compete to be selected by the agent, rather than the consumer.”

Then there’s AI-powered search, which mixes traditional web browsing with generative AI synthesis. Using technologies like AI Overviews and AI Mode shortens the path to purchase and opens the door for dynamic, context-driven advertising.

Finally, businesses will be able to embed brand agents into their digital storefronts. These on-site AI concierges can use a visitor’s unique context to guide them to their perfect product. This boosts conversions while the company retains full ownership of the customer relationship.

3. Adaptive customer experiences

Today, only 21% of banking customers are satisfied with personalisation efforts. The next wave of AI addresses this by shifting customer journeys from static paths to real-time, agentic experiences driven by contextual data, like product searches or live user behaviour.

By leveraging Gemini Enterprise Agent Platform, finance firms can deploy specialised AI agents at scale. They act on a best-practice framework called Generative UI, where the AI doesn’t just interact with a person, but dynamically renders custom interface components — like personalised mortgage calculators or onboarding modules — on the fly. This fuels continuous feedback loops that learn from people’s clickstream behaviour and preferences to tailor interface redesigns without manual coding.

Innovate Finance’s head of regulatory affairs, Andy Thornley, says this evolution opens up some exciting opportunities to build truly proactive customer experiences.

“Instead of waiting for people to tell them what they want, organisations can adapt in real-time to create personalised spaces that stay one step ahead of customer needs,” he explains. “This makes welcoming new customers easier, smoothing out the onboarding process with tailored content that builds confidence and improves marketing ROI.”

Beyond that, understanding a customer’s true intent allows institutions to offer the right services at the perfect moment. And putting a customer’s immediate needs ahead of generic promotions shows them they are genuinely valued, the quickest way to build lasting trust and loyalty.

Social Module

Share